my personal money rules

.png)

I became a financial planner in summer 2020.

Instead of working with old rich people, my mission was to educate my generation about personal finance.

We’re growing up in an entirely different world than our parents, which means the lessons & tactics that might’ve worked for them probably won’t work for us.

There are several timeless lessons - such as “spend less than you make” or "don't try to keep up with the Joneses".

But these are a few personal money rules I’ve developed for myself over the past few years:

Rule 1) If it saves time, spend the money

I’d rather spend money than spend time.

One is wildly infinite and the other, dangerously (yet calmly) scarce.

While I’m not going to alter my savings or put myself in debt to save time, I’ve started to spend more on “convenience” in the past couple of years.

A few examples of this:

- Paying a CPA to file taxes

- Paying an attorney service to file business registrations

- Upgrading to YouTube Premium with no ads

- Subscribing to a design template tool (to save time on basic layout structure)

- Paying for the highest speed internet service (my entire business is online - I can’t even imagine the time savings here)

Rule 2) If it creates a memory, spend the money

Most financial planners preach about saving and investing money.

But I think spending money is just as important, which is why my first two rules have nothing to do with budgeting or the stock market.

I didn’t start a business to follow the traditional retirement path.

I started a business to find a balance between meaningful work and freedom. For me, that means enjoying my money along the way.

For example, I made about $35,000 after-tax in 2022 and I traveled to New York twice.

Sure, there were better places to spend a couple thousand dollars. But the memories I made and the impact those trips had on my life is irreplaceable.

So anything that I believe will create a memory—especially with family—goes to the top of my spending priority list.

Rule 3) Maintain a one year cash reserve

While I love spending money, you still have to practice good financial habits.

I traveled twice, but I also built my cash reserve to $10,000 - a goal I’d been working on for two years. I'm not at a full year yet, but I'm working towards it.

If you have a year of expenses set aside, then your back isn’t always against the wall.

This lets you create with confidence and freedom.

You'd be surprised at what just a little bit of savings can do for your mental health if you've been operating on zero for awhile. I've been there - I'm still transitioning into it right now. I can't imagine what a year of savings will feel like.

Rule 4) Budget & aim for monthly travel

Travel doesn’t have to be a flight to a different country or a trip to Miami.

It could be as simple as a short drive to go camping.

Or a quick roadtrip to the nearest unfamiliar town.

Either way, travel's an important part of my life and dedicating a portion of my earnings to something that's guaranteed to make a memory is a no-brainer.

Rule 5) Insure for security, and nothing more

I’m not insuring my flights, my phone, or my dog. If the sole purpose isn’t security, my money is better spent elsewhere and if anything happens, I’m okay with eating the cost.

Health insurance? Perfect.

Term life insurance? Yes.

Disability? Once affordable.

Car? Liability-only.

Dental? As a self-employed person, right now, no. The potential cost of care doesn’t outweigh paying extra premiums at the moment - same with vision.

Whole life insurance? Nope. However, I’ll reevaluate my rules if I somehow make multiple millions and have excess cash.

Rule 6) Invest or save at least 10% of income

If you’re making enough to cover your standard cost of living, you should be saving something each month. For me, the minimum is 10%.

As my income grows, I plan to raise it to 20%.

That money will automatically be transferred to an investment or savings account each month before I spend any money. This ensures that I’m saving for my future while easily being about to spend guilt-free.

Why?

Because if you’re saving the appropriate amount of money before spending elsewhere, your needs are taken care of.

If investing 10% of your income means that you’ll hit your retirement goals, why wouldn’t you spend the rest of your money how you’d like?

You need to do some planning to determine which numbers are appropriate for your situation, but I struggle with the idea of investing for the future while also enjoying your money today, which is why I don’t have a higher percentage or a strict rule set here.

I don’t know how long I have on this planet, so I’m going to do my best to spend with intention today and save for freedom & flexibility in the future. If you’re in the same boat, I recommend reading Die with Zero by Bill Perkins.

Rule 7) Always tip at least 25% (aim for 2x the cost)

I’ve been a service worker.

I know what it’s like to be on the other side of a $50+ tip.

It’s an indescribable feeling when you’re in a tough spot financially.

I believe that money is energy, and if I can transfer that feeling to someone who may need it, it’s worth it to me.

- Tips apply to wait staff, Uber drivers, barbers—anyone providing a true service

- Bonus: ALWAYS give money to street musicians & artists

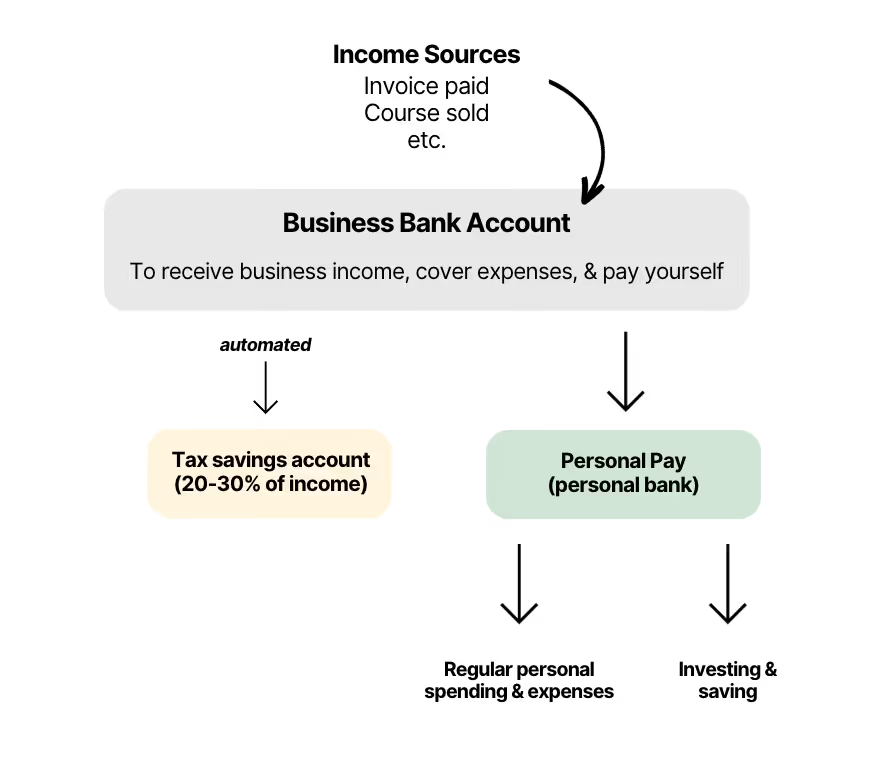

Rule 8) Reduce friction, stay organized, & simplify where possible

I want to spend the least amount of time managing my money as possible.

This means creating systems and simplifying as much as I can.

What does this look like?

Bank accounts:

- 1 primary checking (for all personal income and expenses)

- 1 savings account for my emergency fund

- 1 savings account for travel

- 1 savings account for taxes

Investment accounts:

- 1 taxable investment account

- 1 Roth IRA

- 1 Solo 401(k)

Debts:

- None (but would consider consolidating if there were multiple high-interest debts)

Document storage:

- Google drive for digital documents

- A simple 5 folder binder for physical documents

- I like to have folders in each for: Taxes, Insurance, Relevant Receipts (car repair, donations, etc), Account Statements, Legal documents (business docs, estate docs, etc.)

As far as systems go, I have a relatively simple way to view & manage my cash flow:

All of my businesses receive income in their own bank accounts, I withhold necessary taxes in one account and pay myself so that all income goes to my primary checking account. Then, percentages are distributed to where they need to be (to my emergency fund, investments, etc).

Rule 9) Avoid non-cash flowing debt

I don’t want to waste money by paying interest on a maxed out credit card, new car, or an Instagram-worthy house.

For me, if I’m going to take on debt, it’s going to serve a specific purpose.

The easiest example is investing in real estate:

If I was to buy a 4-unit apartment building, I wouldn’t pay all cash. I’d take out a loan, get charged interest, and be forced to make monthly payments. BUT, because the purpose of buying the building would be an investment, it should be providing some form of cash flow (i.e. money coming back to you) - typically in the form of rent from tenants. The cash flow would then help cover the cost of the mortgage payments.

I doubt I'll ever get into real estate, but it's an area where debt can used advantageously.

I’ve avoided credit card debt, driven the same car for the past 10 years, and rent an apartment so right now, I’m successfully avoiding "bad" debt and I’m extremely happy with the decision so far.

At some point, I’ll likely want to buy a house for non-investment purposes and if it makes financial sense at the time, I’ll happily break this rule.

Rule 10) No more than two actively used credit cards

This relates to the “simplify” step, but it serves as a friendly reminder to not play the points game.

I love free things, but I can confirm that it’s better for *me* to stick with my primary cards and keep my mental space clear from trying to remember which cards I have, their balances, which ones have better points, where to spend each different card, which ones have multipliers - it’s too much.

I’ve tried to take advantage of bonuses and points three times and twice—TWICE—I forgot about the card, left a small balance on it accidentally, and ended up having to pay interest.

Props to the people who can churn cards and get free points all the time.

But I’ll keep avoiding the “How I Traveled to Europe for $32 and You Can Too” articles, swipe my Sapphire Preferred, and just make more money instead.

Rule 11) One to rock, one to stock

In other words, if you like something or it could have collectible value, buy (at least) two.

You’ll never regret having an extra item of something you love—especially when you go to buy another, only to find out it was discontinued.

.avif)

Originally published January 5, 2023

.jpg)

.jpg)

%20(12).avif)

.avif)

.jpg)

.avif)

.jpg)

.jpg)

.avif)